Sometimes the most exciting exploration stories emerge not where no one has ever looked, but where someone stopped too early decades ago. This exact constellation could now be developing at the Gold Standard Project of Storm Exploration (TSXV: STRM; FSE: L840) in northwestern Ontario. The company has announced a targeted exploration and drilling program for 2026 on a roughly five-kilometer-long conductivity target interpreted as a potential VMS system. VMS stands for volcanogenic massive sulphide—deposits that rank among the most sought-after copper, zinc, silver, and in some cases gold deposits worldwide.

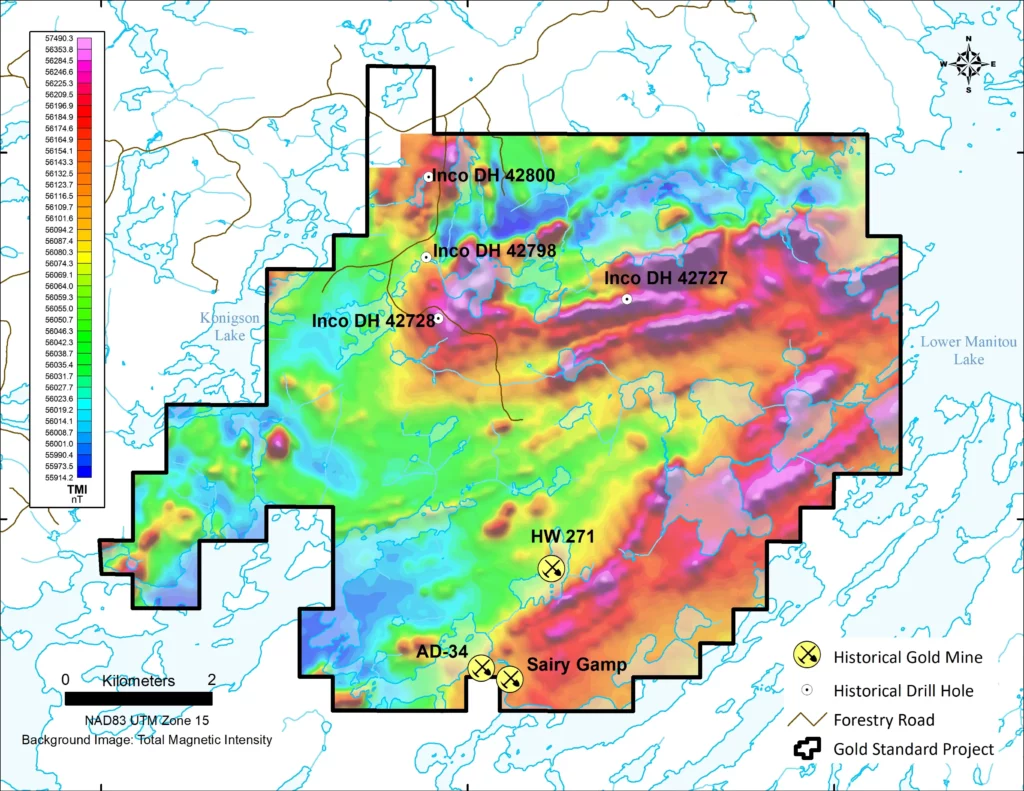

The particular appeal lies in the historical background: As early as the late 1960s and early 1970s, the then International Nickel Company of Canada, or Inco for short, drilled at Gold Standard. Four short drill holes intersected significant sulphide mineralization at that time, including copper and zinc sulphides. However, because the target apparently did not immediately show the nickel character they were seeking, it was not pursued further. Even more remarkable: the drill holes were all less than 50 meters deep, and no assays were performed. In other words: Inco found sulphides but never systematically verified what metal grades were actually present.

Old Inco Trail Only Becomes Visible Today

The irony of the story is hard to overlook. Inco, once one of Canada’s leading resource companies, had apparently identified the target through its own airborne survey and subsequently drilled exactly where Storm now sees a strong EM anomaly. However, since the EM data from that time were never publicly available, it remained unclear to later explorers why these historical drill holes were placed at precisely these locations. The target was simply invisible to the market.

Only Storm’s project-wide VTEM survey from 2022 made the connection visible again. The data show a roughly five-kilometer-long conductivity anomaly that can be up to 100 meters wide and extends along a favorable geological structure in the northern part of the Gold Standard property. Storm interprets this anomaly as a potential VMS system. Crucially: conductivity alone does not prove an economic deposit. However, it can be an important indicator of conductive sulphide minerals. This fits precisely with the historical observations in the Inco drill cores, which described pyrrhotite, pyrite, chalcopyrite, and sphalerite. Chalcopyrite is a copper mineral, sphalerite a zinc mineral.

According to Storm’s announcement today, Inco drill hole 42800 intersected a 21-meter-thick section with alternating massive sulphides and sulphide stringers, including pyrrhotite, chalcopyrite, and sphalerite. Drill hole 42727 encountered a 19-meter section with massive pyrite and minor chalcopyrite from 14.9 meters depth, followed by disseminated pyrite and minor pyrrhotite to the end of the hole at 44.8 meters. For a target that was only tested with very short, shallow drill holes at the time, this is geologically an unusually strong finding.

The Real Question Is: Just Copper-Zinc—or Gold as Well?

The name Gold Standard is no coincidence. Roughly four kilometers south of the large EM anomaly are historical gold workings, including Sairy Gamp, HW-271, and AD34. HW-271 is particularly significant for the current VMS thesis because high-grade gold-copper mineralization was described there in the past. Storm reported samples from the HW-271 area in 2022 with up to 166 g/t gold, 197 g/t silver, and 1.47% copper. Additional samples yielded 88.6 g/t gold and 1.49% copper, 83.4 g/t gold and 0.96% copper, and 77.6 g/t gold and 2.59% copper.

This raises the obvious question: Is Gold Standard merely a classic copper-zinc target, or could the regional gold-copper signature also be related to the VMS system? This question is critical for investors. A pure base metal target can already be significantly value-enhancing for a junior explorer. However, a VMS system with additional gold and silver content can trigger an entirely different valuation scenario.

Storm CEO Bruce Counts refers in today’s announcement to two world-class Canadian examples: the Horne Mine in Rouyn-Noranda, Québec, and Kidd Creek near Timmins, Ontario. Horne produced between 1927 and 1989 from 53.7 million tonnes of ore approximately 260 tonnes of gold and 1.13 million tonnes of copper at average grades of 2.22% copper, 6.1 g/t gold, and 13 g/t silver. Kidd Creek, in turn, delivered between 1966 and 2016 a total of 140.4 million tonnes of ore with grades of 2.29% copper, 6.15% zinc, and 86.2 g/t silver. Such comparisons are of course not a forecast for Gold Standard. However, they demonstrate why VMS targets in Canada can be so attractive for exploration companies: when they work, they can be large, polymetallic, and extremely valuable.

Modern Exploration Meets an Almost Untested Target

Storm is now planning a two-phase program. Initially, ground geophysics, mapping, prospecting, and soil sampling will improve the resolution of the EM anomaly and define the best drill targets. Drilling will follow. According to today’s company announcement, 10 to 15 core drill holes totaling 2,000 to 3,000 meters are planned. The objective is to test for the presence of precious metals and critical metals, as well as to better understand the dip and thickness of the mineralization. Field work is scheduled to begin after snowmelt in early June; the drilling program is expected to commence in early July, once the supporting data have been evaluated.

This is an important point: Storm does not have to start from scratch. The historical Inco work has already confirmed sulphides. The modern VTEM data now provide the geophysical framework. The 3D interpretation suggests that the stronger conductivity does not necessarily lie at surface, but at greater depth, approximately around 100 meters. This is precisely where the historical shallow drill holes never really tested. Inco essentially only scratched the surface. Storm now intends to test for the first time with a modern, systematic drilling program whether a coherent and potentially mineralized VMS system exists below the historical intersections.

Gold Standard Could Be the Near-Term Catalyst in the Storm Portfolio

Storm Exploration meets many criteria that speculative resource investors look for in a junior explorer: a manageable valuation, a tight share structure, experienced management, and multiple projects with discovery potential. Gold Standard is just one of three projects the company holds in northwestern Ontario. Keezhik and Attwood also possess gold potential and are located in an area that has recently come back into focus for explorers.

The difference with Gold Standard, however, lies in the potential near-term catalyst. While many juniors still need to define a target, Storm already possesses a large-scale EM anomaly, historical sulphide drill holes, and high-grade gold-copper samples nearby. This is a rare combination. Should the planned drilling program confirm that the conductivity anomaly is indeed caused by massive or semi-massive sulphides, the market will likely need to revalue the project. Should gold also be confirmed in the system, the story would intensify significantly.

Conclusion: Inco Stopped Before the Real Question Was Asked

Gold Standard is a classic “unfinished business” story. Inco found significant sulphide mineralization more than 50 years ago, but was apparently searching for nickel, left the drill cores unassayed, and did not publish the critical EM data. As a result, the target disappeared from view for decades. Only Storm Exploration has made the old trail visible again with modern geophysics. For a company with only approximately CAD 4 million market capitalization, even the confirmation of a credible VMS system could trigger a massive re-rating. Gold Standard remains an early-stage exploration target, and conductivity is no substitute for drill results. However, the starting position is unusually strong: five kilometers of strike length, historical copper-zinc sulphides, high-grade gold-copper samples just a few kilometers away, and a first genuine modern drilling program in sight. It is precisely such constellations from which disproportionate revaluations can emerge in the junior sector.